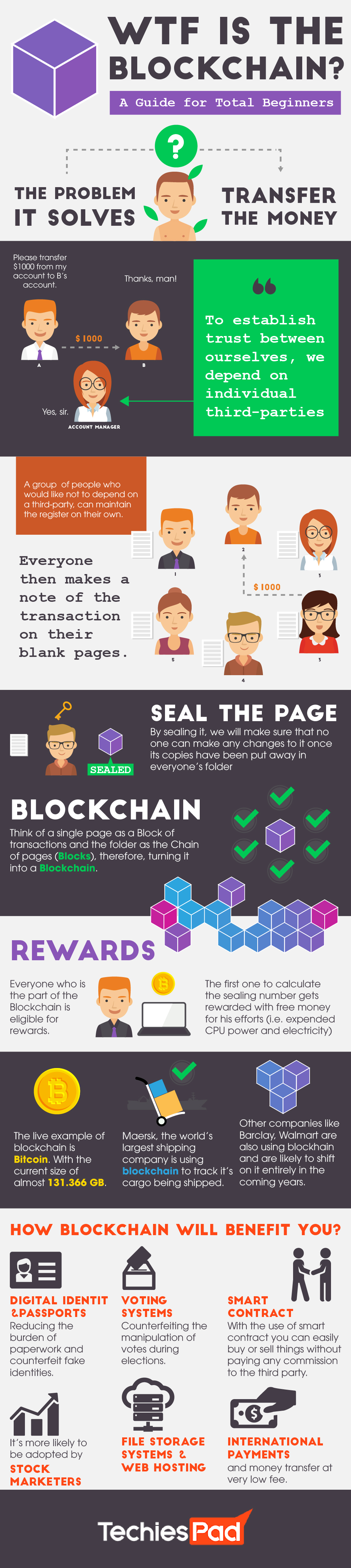

The internet economy is not just restricted to e-retail websites like Amazon. A big chunk of online transactions today takes place through blockchain technologies, the most popular of which is Bitcoin. And it becomes easy to see why that share of the market has been growing over the years. Blockchains are oblivious to geographies, nationalities and other boundaries, making the market freer than it has ever been before.

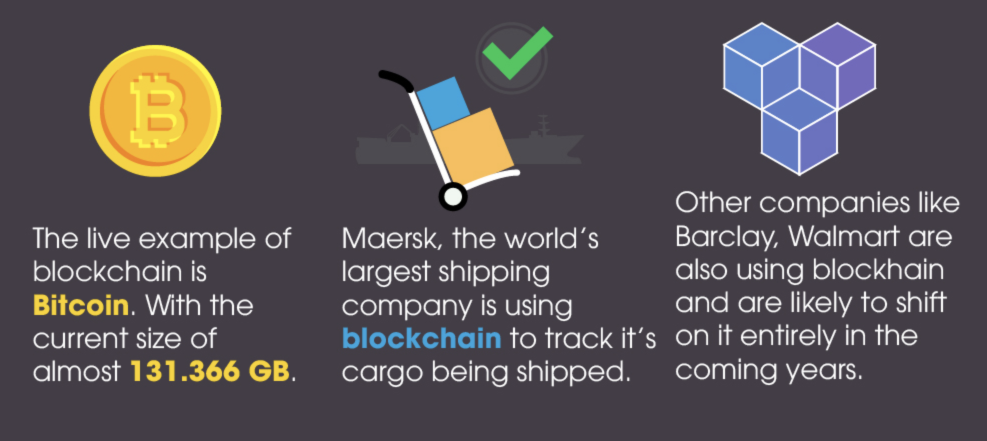

Blockchains have been around for a long time, originating from cryptography back in 1999. And it holds potential that goes far beyond monetary transactions. The technology has been implemented by giants like Maersk to track deliveries. Others have found it useful to maintain inventories. The unique selling proposition of the technology in all cases, however, remains the same. It is incredibly accountable and aids transparency between the parties involved.

It is surprisingly simple to understand how the technique works. Consider a bank passbook. The bank keeps a record of how much money you hold and to whom you transferred it in the past. A blockchain can be like that, but it is much safer. A record on a blockchain is made unalterable when it is generated. And when you consider that it is replicated to multiple sources, the sense of security is multiplied, too.

When you make a sale or purchase on the internet, the blockchain records it in a page of data that cannot be tampered with. This is then replicated to many devices that are part of the blockchain. Altering one record is a tough nut to crack. Altering so many unmarked copies of the transaction that are potentially located all over the world is not just hard, it is virtually impossible.

TechiesPad has a neat infographic to explain more about the technology and how it is changing the face of the business world. Check it out below.

Author Bio: Stacy Miller has been blogging ever since she was in high school. Her love for technology and disdain for generic Hollywood movies has only grown over the years.